Published as part of the ECB Economic Bulletin, Issue 4/2022.

Russia’s invasion of Ukraine has significantly increased uncertainty in the euro area. While the very high energy prices and renewed supply shortages resulting from the war are key observable factors affecting economic activity, a third unobservable factor – the associated rise in uncertainty – is also playing a major role. The economic literature defines an uncertainty shock as an outcome of a random event (such as a war) that makes the economic outlook less predictable.[1] As a result of such an increase in uncertainty, economic confidence declines, leading to cuts in the expected spending of households and businesses. This box aims to study the macroeconomic implications of the heightened uncertainty in the euro area that has been triggered by the invasion of Ukraine, focusing on GDP, domestic demand (such as business investment and consumption) and developments in major individual sectors (such as manufacturing and services, and durable and non-durable goods).

Uncertainty affects the economy via a number of different channels. One channel frequently cited in the literature relates to the “irreversibility of investment”.[2] Investment is often very difficult to reverse, given the associated fixed costs. Rising uncertainty can therefore lead firms to delay and/or forgo investment, with a view to making better‑informed investment decisions once the economic outlook is clearer. A second channel is associated with “precautionary savings”.[3] In response to an uncertainty shock (which can negatively affect future income), households seek to save more and consume less. A third channel relates to the interplay between heightened uncertainty and financial “frictions” (such as borrowing constraints), which can have powerful effects on economic activity, with financial conditions for firms and households typically tending to deteriorate after an uncertainty shock.[4]

A Structural Vector Autoregression (SVAR) model with sign and narrative restrictions is used to identify uncertainty shocks (Chart A). Various approaches have been used to identify such shocks in the literature. It is typically assumed that sudden changes in variables other than uncertainty do not affect uncertainty contemporaneously.[5] However, causality can operate in both directions: for example, uncertainty shocks affect economic activity, but adverse shocks to output (i.e. negative demand shocks) are also likely to increase uncertainty. This box identifies uncertainty shocks using a SVAR model with sign and narrative restrictions, which considers this contemporaneous relationship between variables. Specifically, the model incorporates the Harmonised Index of Consumer Prices (HICP), monthly interpolated GDP, the ten-year overnight index swap (OIS) rate, corporate bond spreads and the Composite Indicator of Systemic Stress (CISS).[6] The latter is used to identify uncertainty shocks through narrative restrictions, by assuming that the uncertainty shock explains most of the dynamics of the CISS in September 2001 (the terrorist attack on the World Trade Center in New York) and August 2007 (the interbank credit crisis).[7]

Chart A

The CISS and uncertainty shocks

(left-hand scale: CISS index (0 = lowest level of financial stress; 1 = highest level); right-hand scale: standard deviation)

Sources: ECB and ECB calculations.

Notes: The SVAR model was estimated for the period from January 1999 to December 2019, identifying cost-push, demand, interest rate, financial and uncertainty shocks. The variables incorporated in the model are the HICP, monthly interpolated GDP, the ten‑year OIS rate, corporate bond spreads and the CISS. Sign and narrative restrictions are in line with the approach adopted in Antolín‑Díaz, J. and Rubio-Ramírez, J.F., “Narrative Sign Restrictions for SVARs”, American Economic Review, Vol. 108, No 10, 2018, pp. 2802‑2829. The latest observations are for April 2022.

The model is estimated for the period from January 1999 to December 2019 (i.e. excluding the coronavirus crisis, as macroeconomic time series have seen major structural breaks following the onset of the pandemic). The estimated elasticities are then used to quantify uncertainty shocks in the period up to April 2022. The model is able to capture major events which led to a rise in uncertainty, such as the invasion of Iraq in March 2003 and the collapse of Lehman Brothers in September 2008, as well as episodes from the euro area sovereign debt crisis. The estimated uncertainty shocks line up well with past political, geopolitical and economic events that would typically be associated with high levels of uncertainty and, likewise, the recent intensification of uncertainty coincides with the ongoing war in Ukraine. The uncertainty shock in March 2022 following the Russian invasion of Ukraine has an estimated size of around six standard deviations, making it the second-largest shock on record (after the episode in March and April 2020 on account of the pandemic).

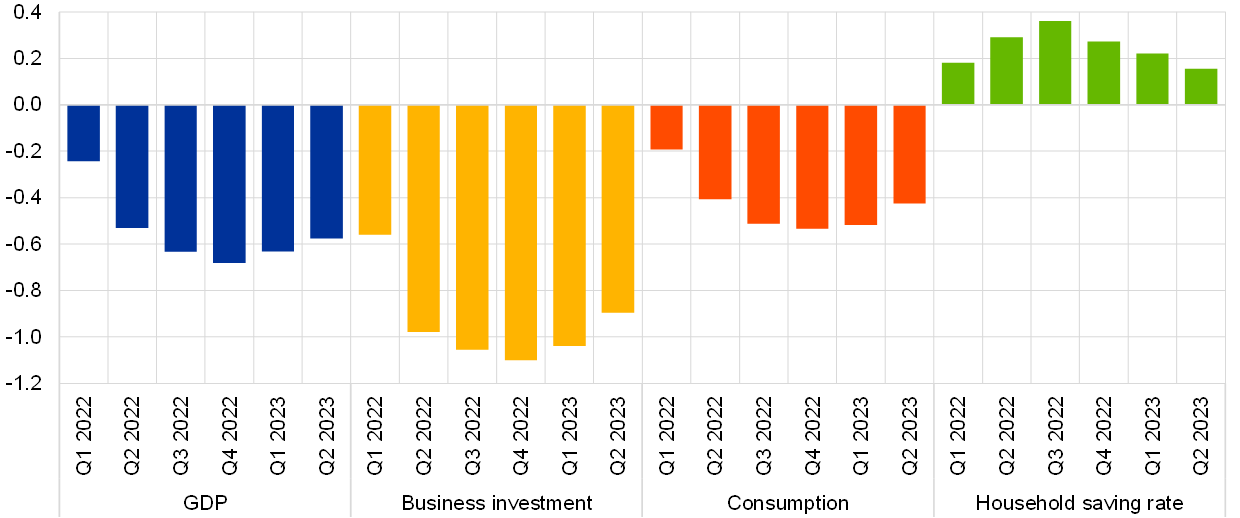

Uncertainty shocks negatively affect GDP and domestic demand, with a larger impact on business investment than on consumption. Once uncertainty shocks have been identified using the SVAR model, a “local” projection framework can be used to estimate the impact that those shocks have on euro area GDP and its demand components, the household saving rate and value added in the manufacturing and services sectors.[8] The local projection approach is typically used when shocks are assessed as being exogenous to the variables of interest. The estimated uncertainty shock in the period from February to April 2022 is expected to reduce euro area GDP relative to the level projected by the model in the absence of any shocks (the “trend” level), reaching a trough of about 0.7% in the fourth quarter of 2022 (Chart B, panel a). The increase in uncertainty is expected to weigh on the spending decisions of households and firms, with the household saving rate rising by about 0.4 percentage points in the third quarter of 2022. The elevated uncertainty is expected to have a stronger impact on business investment than consumption, with the two demand components being reduced by 1.1% and 0.5% respectively in the fourth quarter of 2022 relative to their trend levels.

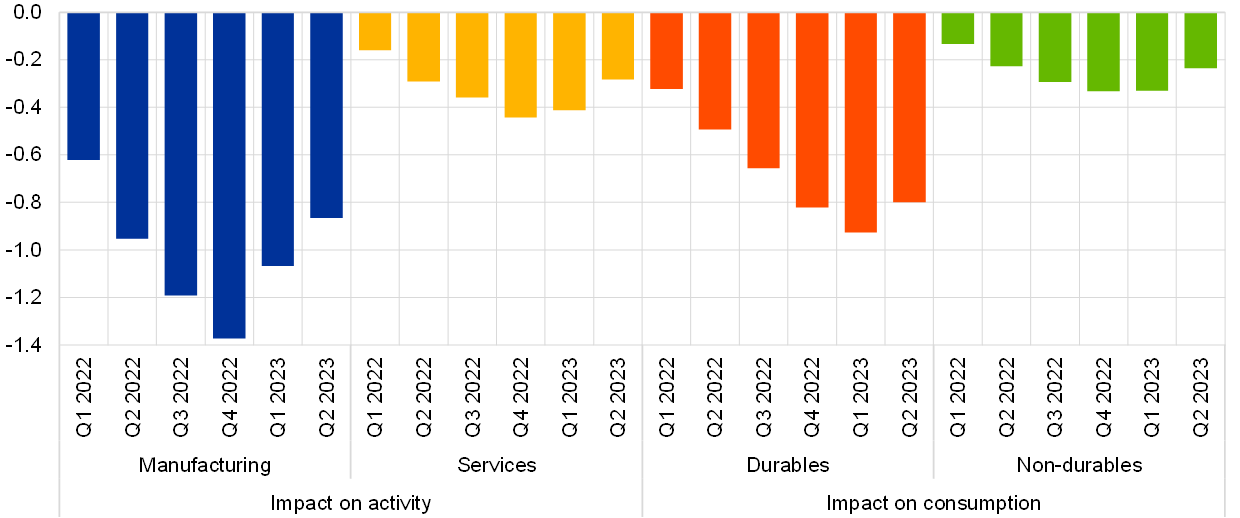

At a sectoral level, the uncertainty shock is expected to affect manufacturing more than services and to have a stronger impact on sectors producing goods with longer lifespans (Chart B, panel b). The larger impact on manufacturing could stem from the fact that manufacturing output has, historically, been more prone to cyclical swings and is more dependent on energy inputs (which also exhibit significant volatility across cycles). Looking at the composition of consumption, durable goods are more affected by uncertainty shocks than non‑durables, consistent with the fact that spending on durables can be postponed in response to adverse shocks, as existing stocks of durable goods can still provide utility given their longer lifespans.[9] Indeed, the effect on durable goods is three times the size of the impact on non-durables.[10] Overall, the war and the rise in energy prices have made the economic outlook more uncertain, especially in energy-dependent sectors and in sectors producing goods with longer lifespans.

Chart B

Macroeconomic impact of the uncertainty shock associated with Russia’s invasion of Ukraine

a) Impact on GDP, business investment, consumption and the household saving rate

(percentages and percentage points; deviation from trend levels)

b) Impact on manufacturing, services, and durable and non-durable goods

(percentages; deviation from trend levels)

Sources: Eurostat and ECB calculations.

Notes: The impact has been estimated by means of a local projection framework, using the uncertainty shock identified by the SVAR model and controlling for all the variables included in that model. The elasticities estimated over the period from the first quarter of 2000 to the fourth quarter of 2019 and the size of the estimated uncertainty shock between February and April 2022 have been used to derive the overall impact on economic activity. Output and prices were expressed using quarter-on-quarter growth rates, while financial variables were expressed using quarterly first differences.

See Jurado, K., Ludvigson, S.C. and Ng, S., “Measuring uncertainty”, American Economic Review, Vol. 105, No 3, 2015, pp. 1177-1216; and Scotti, C., “Surprise and uncertainty indexes: Real-time aggregation of real-activity macro-surprises”, Journal of Monetary Economics, Vol. 82, 2016, pp. 1-19.

See Bloom, N., “The impact of uncertainty shocks”, Econometrica, Vol. 77, No 3, 2009.

See Basu, S. and Bundick, B., “Uncertainty shocks in a model of effective demand”, Econometrica, Vol. 85, No 3, 2017.

See Christiano, L.J., Motto, R. and Rostagno, M., “Risk shocks”, American Economic Review, Vol. 104, No 1, 2014; and Gilchrist, S., Sim, J.W. and Zakrajšek, E., “Uncertainty, financial frictions, and investment dynamics”, NBER Working Papers, No 20038, 2014.

For the United States, see Bloom (2009, op. cit.), Jurado et al. (2015, op. cit.) and Scotti (2016, op. cit.). For the euro area, a Choleski approach is used in the box entitled “The impact of the recent spike in uncertainty on economic activity in the euro area”, Economic Bulletin, Issue 6, ECB, 2020. For a detailed comparison of the standard Choleski framework and a proxy structural vector autoregression (SVAR) approach, see Bobasu, A., Geis, A., Quaglietti, L. and Ricci, M., “Tracking global economic uncertainty: implications for the euro area”, Working Paper Series, No 2541, ECB, 2021.

For more information on this index, see Holló, D., Kremer, M. and Lo Duca, M., “CISS – a composite indicator of systemic stress in the financial system”, Working Paper Series, No 1426, ECB, 2012.

Bloom (2009, op. cit.) refers to the terrorist attack of 11 September 2001 as a key uncertainty event. In the interbank credit crisis of August 2007 severe liquidity issues affected financial markets following the decision by BNP Paribas on 9 August 2007 to freeze three funds exposed to the US subprime mortgage market. At that point investors recognised the need – and their inability – to assess which intermediaries holding mortgage-related instruments were stuck with the toxic components. The same challenge applied to the market for repurchase agreements (repos), where economic agents were using these instruments as collateral for short-term loans. The interbank market, which provides liquidity to banks around the world, dried up largely owing to fear of the unknown.

The technique involves regressing contemporaneous information on variables of interest in successive periods ahead, see Jordà, O., “Estimation and Inference of Impulse Responses by Local Projections”, American Economic Review, Vol. 95, No. 1, 2005, pp. 161–182.

See Browning, M. and Crossley, T.F., “Shocks, stocks, and socks: smoothing consumption over a temporary income loss”, Journal of the European Economic Association, Vol. 7, No 6, 2009, which shows that, in the short run, households can cut their total expenditure without a significant fall in welfare if they concentrate on reducing their purchases of durables.

The European Commission survey on uncertainty corroborates qualitatively the econometric results. The survey asks managers and consumers to indicate how difficult it is to make predictions about their business situation and household finances. Since the war started in February 2022, uncertainty has increased more in industry than services. The most affected sectors have been construction and manufacturing. Consistent with the findings from the empirical model, uncertainty in the durable goods subsector has been more affected than uncertainty in the non-durable goods subsector.