The role of bank and non-bank interconnections in amplifying recent financial contagion

Published as part of Financial Stability Review, May 2020.

Recent events have shown that stress in non-banks can affect other parts of the financial system, for example through forced asset sales and reduced short-term funding. This box examines the interconnections between banks and non-banks through direct exposures, overlapping portfolios and ownership links, and considers how these can increase the risk of systemic contagion.

Significant financing links between banks and non-banks

Sources: ECB (large exposure data and securities holdings statistics) and ECB calculations.Notes: The right panel shows the aggregate exposures of the largest euro area banks towards global investment funds and insurance corporations. Securities include debt securities, investment fund shares and equity. Loans are reported if the exposure is above the threshold of 10% of Common Equity Tier 1 capital. The horizontal axis shows the domicile of the bank.

Non-banks and banks are important funding sources for each other, leading to sizeable direct exposures. Euro area insurance corporations and pension funds (ICPFs) hold around 15% of euro area bank bonds, while investment funds (IFs), money market funds (MMFs) and other financial institutions (OFIs) together hold around 24% of the market (see Chart A, left panel). Within this, MMFs play a particularly important role in short-term funding (see Box 7). Banks also provide credit to insurers and investment funds through direct lending and investment in their securities. For example, the main euro area banking groups held over €11 billion in debt and equity securities issued by insurers and €75 billion in global fund shares at the end of 2019. They also provided insurers and funds with over €57 billion in loans (see Chart A, right panel). The exposures are concentrated in the largest banks, but remain low relative to bank capital in most cases.

Direct links between different types of non-banks are also sizeable. Insurance corporations hold over 25% of their assets in investment fund shares and rely heavily on MMFs for their liquidity management. This meant that pressure on investment funds in March negatively affected insurers’ profitability. For unit-linked insurance policies, insurers also invest in funds whose liquidity profile might not match the daily redemptions often offered to policyholders.[2] This could expose them to liquidity risk, as seen for example in January, when two Irish commercial real estate unit-linked funds had to introduce redemption gates following a substantial rise in outflows, in line with the contractual provisions designed to deal with such an eventuality.

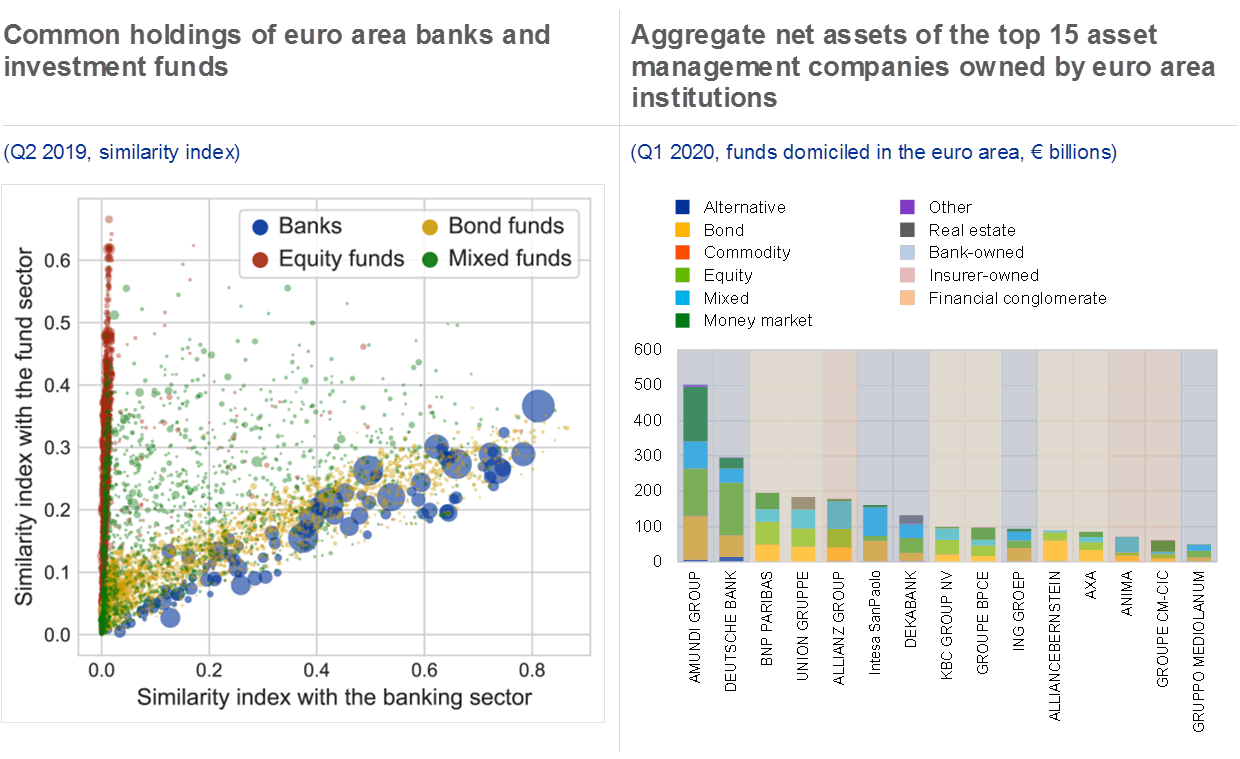

Large asset sales by financial institutions in illiquid markets can propagate stress across the financial system via mark-to-market losses on common exposures. For example, the portfolios of euro area banks and bond funds have significant common exposures, although the latter tend to be more diversified geographically (see Chart B, left panel). Large banks, which are at the core of the interbank network, are particularly exposed to the fund sector. Large common exposures between banks, funds and insurers increase the risk of amplifying market stress if they have to liquidate a large or illiquid part of their portfolios simultaneously.[3] Investors holding the same assets may then suffer mark-to-market losses in their balance sheet, potentially leading to fire sales that increase the cost of market financing for non-financial corporations (NFCs). Market intelligence suggests that large outflows from funds in the US caused forced asset selling in March, particularly into illiquid markets such as those for high-yield and municipal bonds and mortgage-backed securities.

Euro area banks and non-banks are interconnected through common exposures and ownership links

Sources: ECB securities holdings statistics, Refinitiv and ECB calculations.Notes: The left panel is based on the cosine similarity index, which measures the level of commonality between pairs of portfolios (see Getmansky Sherman, M., Girardi, G., Hanley, K. W., Nikolova, S. and Pelizzon, L., “Portfolio Similarity and Asset Liquidation in the Insurance Industry”, working paper, 2019). The index equals zero if the portfolio allocations are uncorrelated and equals one if they are the same. The sample includes 101 banks and 9,393 open-ended mutual funds domiciled in the euro area (4,224 equity funds, 3,060 bond funds and 2,109 mixed funds). Assets are tradable securities and redeemable fund shares. The three different fund types are aggregated to compute the similarity index with the whole fund sector shown on the y-axis. The size of each point is proportional to the portfolio size. The right panel includes assets of mutual funds and exchange-traded funds. Asset managers are classified as owned by banks/insurers when the asset manager is a subsidiary of the bank/insurer (this excludes cases where bank/insurance activities are a subordinate business of the group or where the holding company also holds banks/insurers) or has a bank/insurer as a majority shareholder. The latest observations are for March 2020.

Finally, banks and insurers are often majority investors in large asset management companies and heads of financial conglomerates. Control over such companies allows banks and insurers to diversify their profitability and risks, and exploit economies of scope (see Chart B, right panel). Similarly, financial conglomerates (e.g. French bancassurance companies) allow the sale of insurance and investment products through the banking arm. These links can help to optimise liquidity between the parent company and affiliated institutions and provide long-term benefits in terms of revenue and risk diversification, but may also be a source of contagion in stress periods. Contagion can occur if there are credit lines and contingency arrangements between the holding company and the affiliated institutions or via step-in and reputational risks related to confidence effects or revenue losses.[4] Recent challenges faced by insurance subsidiaries may propagate to the banking parent (and vice versa) as the business models are closely interlinked (i.e. the profitability of parent banks sometimes relies on dividends and returns from insurers) and the parent may need to transfer own funds to the subsidiaries (see Section 4.3).

- [1]Michiel Kaijser, Dominika Kryczka and Luca Mingarelli provided data support.

- [2]See Financial Stability Review, ECB, May 2019, Box 9.

- [3]See Financial Stability Review, ECB, May 2018, Chart 3.26.

- [4]Direct spillover risks within a financial conglomerate are mitigated by the supplementary supervision under the Financial Conglomerates Directive (Directive 2002/87/EC of the European Parliament and of the Council of 16 December 2002 on the supplementary supervision of credit institutions, insurance undertakings and investment firms in a financial conglomerate, OJ L 35, 11.2.2003, p. 1).