Draft budgetary plans for 2021: a review in times of the COVID-19 crisis

Published as part of the ECB Economic Bulletin, Issue 8/2020.

On 18 November 2020 the European Commission released its opinions on the draft budgetary plans of euro area governments for 2021. In contrast to previous years and in the context of the coronavirus (COVID-19) pandemic, this year’s European Commission assessment was of a qualitative nature and did not focus on numerical compliance with the fiscal rules. This was due to the activation of the general escape clause[1] which allows Member States to deviate from the adjustment requirements of the Stability and Growth Pact in certain specific, defined situations, such as a severe economic downturn for the euro area or the Union as a whole. Instead the Commission’s assessment was based on the fiscal country-specific recommendations adopted by the Council on 20 July 2020 as well as its guidance issued in September in the form of letters sent to all Member States indicating that the general escape clause would remain active also in 2021 to ensure the needed support from fiscal policies. The Commission also clarified in its assessment that when economic conditions allow, Member States should pursue fiscal policies aimed at achieving prudent medium-term fiscal positions and ensuring debt sustainability, while enhancing investment. In order to reconcile the need to provide macroeconomic stabilisation while ensuring medium-term fiscal sustainability, the Commission stated that support measures should be targeted and temporary, as permanent measures which are not financed by compensatory measures may affect fiscal sustainability in the medium term.

The draft budgetary plans point to a shift in the composition of measures from emergency to recovery measures in 2021, but do not yet fully reflect support from the Next Generation EU (NGEU). According to the European Commission, Member States have taken sizeable fiscal measures in response to the pandemic amounting to 4.2% of GDP in 2020 and 2.4% of GDP in 2021. The composition of fiscal packages in 2020 largely consisted of emergency measures aimed at alleviating the immediate effects of the crisis, namely to address the public health situation and limit economic scarring. According to the Commission’s assessment, such emergency measures amounted to approximately 80% of 2020 fiscal packages at the aggregate euro area level. From 2021 onwards, the measures related to the provision of emergency support are projected to expire gradually and there is a shift towards measures supporting the recovery. The European Commission’s assessment of the draft budgetary plans points to recovery measures, such as indirect tax cuts and increased government investment, accounting for over 60% of the fiscal measures in 2021. The NGEU, and in particular its central pillar the Recovery and Resilience Facility, is expected to start being implemented in 2021. However, given the state of preparations, especially with respect to national recovery and resilience plans, only minor parts of the revenue and expenditure related to the facility are reflected in the European Commission’s autumn forecast and in some of the draft budgetary plans.

The European Commission indicated that the draft budgetary plans for 2021 are overall in line with the fiscal policy recommendation adopted by the Council, but highlighted risks where measures are planned to be permanent. It assessed that in the majority of the euro area countries the measures for 2021 are (mostly) temporary with only the plans of France, Italy, Lithuania[2] and Slovakia pointing to measures that do not appear to be temporary or matched by offsetting measures. For Belgium, Greece, Spain, France, Italy and Portugal, the European Commission highlighted that “given the level of their government debt and high sustainability challenges in the medium term … it is important to ensure that, when taking supporting budgetary measures, fiscal sustainability in the medium term is preserved”. The large prevailing uncertainty makes it difficult to assess measures, all the more so as temporary and more structural measures cannot always be distinguished, given that countries are adopting measures in response to the evolution of crisis waves.

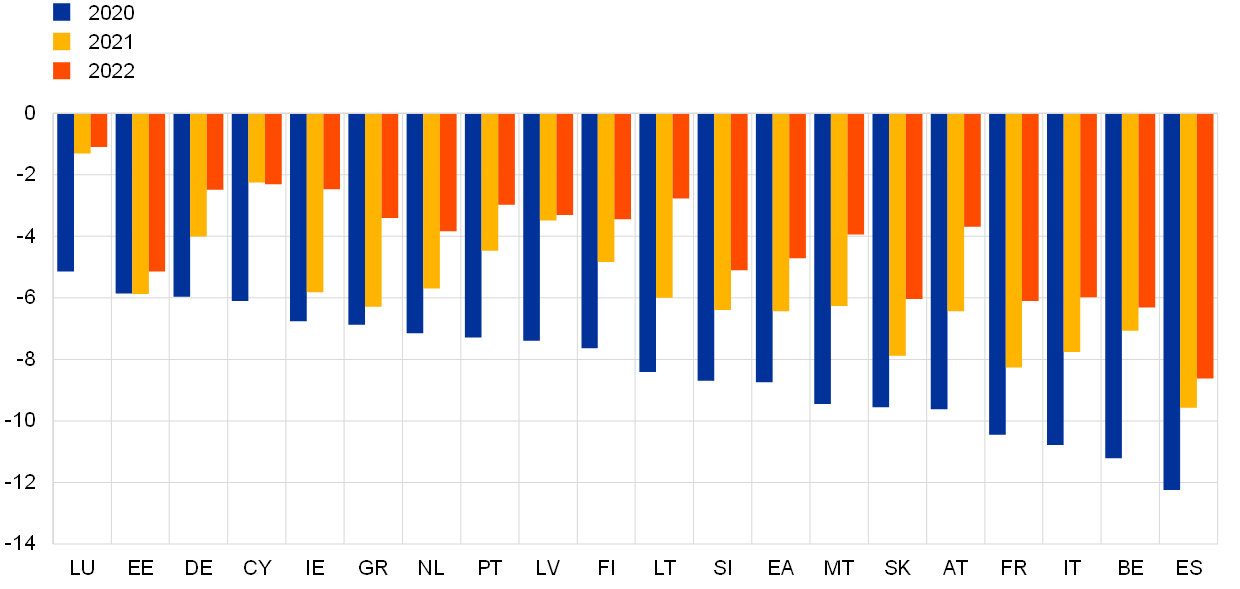

The Commission’s assessment has to be seen in light of the significant and divergent impact that the severity of the COVID-19 shock and the fiscal support measures are having on public finances, but also the prevailing large uncertainty. On average around 30% of the budgetary deterioration projected in 2020 is expected to be reversed in 2021 with deficit ratios remaining above the 3% of GDP threshold in all euro area countries except Luxembourg and Cyprus (see Chart A). Spain, France, Italy and Slovakia are projected to have the highest deficits of more than 7.5% of GDP in 2021. Based on a no-policy-change assumption, deficits would remain above the 3% threshold in thirteen euro area Member States in 2022. Moreover, many countries that entered the crisis with high debt ratios of around 100% and above are projected to be hit strongest by the COVID-19 shock in terms of increasing indebtedness (see Chart B). Only five euro area countries are expected to maintain debt ratios below the Maastricht 60% of GDP reference value in 2022, i.e. Estonia, Latvia, Lithuania, Luxembourg and Malta.

Chart A

General government budget balances, 2020-22

(percentages of GDP)

Sources: European Commission (AMECO database) and ECB calculations.

Chart B

General government gross debt, 2019-22

(percentages of GDP)

Sources: European Commission (AMECO database) and ECB calculations

The European Commission does not intend to trigger excessive deficit procedures at the current stage in response to breaches of the 3% of GDP deficit reference value and the debt rule. Currently, only Romania is subject to an excessive deficit procedure (EDP) ‒ since April 2020. In its November package, the Commission stated that in light of the “exceptional uncertainty created by the outbreak of COVID-19 and its extraordinary macroeconomic and fiscal impact, including for designing a credible path for fiscal policy a decision on whether to place Member States under the Excessive Deficit Procedure should not be taken”. With the same reasoning, the European Commission indicated that no decision on further steps in Romania’s EDP, which had been launched in April 2020 based on the 2019 budgetary deficit, could be taken at this juncture. It assessed, however, that in Romania, “Important underlying drivers of the fiscal situation that were already present before the pandemic struck in 2020, have not been modified”. The European Commission will reconsider the opening of additional EDPs in spring 2021, on the basis of validated data for 2020 and its 2021 spring forecast.

In view of the sharp contraction in the euro area economy, an ambitious and coordinated fiscal stance remains critical until a durable recovery is in place that will allow the rebuilding of prudent medium-term fiscal positions. Following a highly expansionary fiscal stance in 2020, the European Commission’s 2020 autumn forecast points to a phasing-out of emergency measures, however fiscal support is still projected to remain substantial with the adoption of new measures targeted at supporting the recovery. As long as the health emergency persists and the recovery has not become self-sustained, it will be important that temporary measures are extended to avoid cliff-edge effects. This notwithstanding, it is crucial that measures are timely, temporary and targeted so as to deliver fiscal support in the most effective manner while not creating persistent effects on budgetary positions in the post-crisis period and thus ensuring fiscal sustainability. When epidemiological and economic conditions allow, attention should shift to pursuing fiscal policies aimed at achieving prudent medium-term fiscal positions, while enhancing investment. In this respect, the NGEU provides an opportunity to support investment and contribute to a sustainable recovery.

- The clause was introduced as part of the “Six-Pack” reform of the Stability and Growth Pact in 2011. The clause can be activated in the case of an unusual event outside the control of the Member State concerned, which has a major impact on the financial position of the general government or in periods of severe economic downturn for the euro area or the Union as a whole. When activated it allows Member States to temporarily depart from the fiscal adjustment requirements under both the preventive and corrective arms of the Pact provided this does not endanger fiscal sustainability in the medium term.

- Lithuania submitted a no-policy-change scenario draft budgetary plan.