- PRESS RELEASE

Survey on the Access to Finance of Enterprises: firms report moderate tightening of financing conditions

8 April 2024

- Euro area firms reported that financing conditions tightened further in the first quarter of 2024, but much less so than in the fourth quarter of 2023.

- Firms reported a modest reduction in the need for bank loans, while fewer firms reported a reduction in the availability of bank loans. As a result, the increase in the financing gap was smaller than in the previous survey round.

- Fewer enterprises reported an increase in turnover over the last three months, but firms were more optimistic on developments in the next quarter. Cost pressures remained widespread across size classes but declined somewhat – particularly for interest expenses.

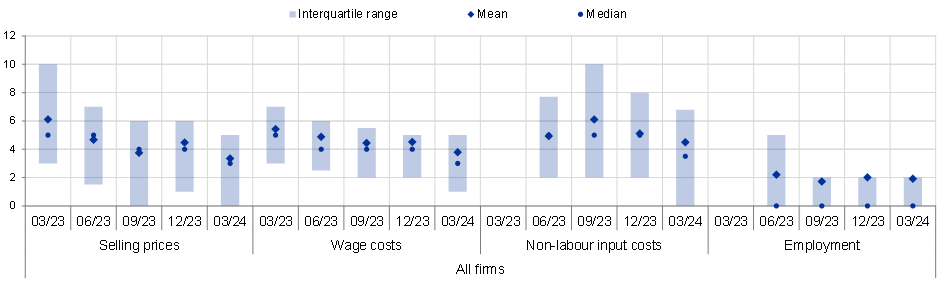

- Firms expected their selling prices and wages to increase by averages of 3.3% and 3.8% respectively in the next 12 months, with both figures representing a moderation relative to the previous survey round.

- Firms’ inflation expectations declined, with their median expectations for annual inflation in one, three and five years standing at 3.4%, 3.0% and 3.0% respectively. Firms considered that risks to the inflation outlook in five years were tilted to the upside, rather than the downside.

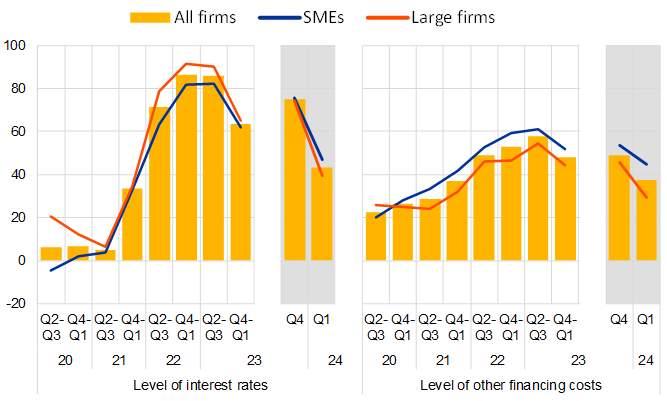

The results of the 30th round of the Survey on the Access to Finance of Enterprises (SAFE) suggest that euro area firms’ financing conditions tightened further in the first quarter of 2024, but less so than in the fourth quarter of 2023. The net percentages of firms reporting increases in interest rates on bank loans and increases in other financing costs (i.e. charges, fees and commission) both declined strongly, falling to 43% (after 75% in the previous quarter) and 37% respectively (after 49% previously, Chart 1).

A net 1% of firms reported a decline in the need for bank loans in the first quarter of 2024, compared with a net 4% signalling increases in the fourth quarter of 2023. At the same time, fewer firms reported a decline in the availability of bank loans, with a net 3% of firms indicating a deterioration, down from 9% in the fourth quarter of 2023. Thus, the increase in the financing gap was smaller than in the previous survey round. Looking ahead, firms have become more optimistic about the availability of bank loans over the next three months.

Firms perceived the general economic outlook to be the main factor hampering the availability of external financing, albeit slightly less so than in the previous survey round (with a net percentage of -26%, down from -32%). At the same time, their perceptions of banks’ willingness to lend, which reflect banks’ risk aversion, improved further (with a net percentage of 4%, up from 1%).

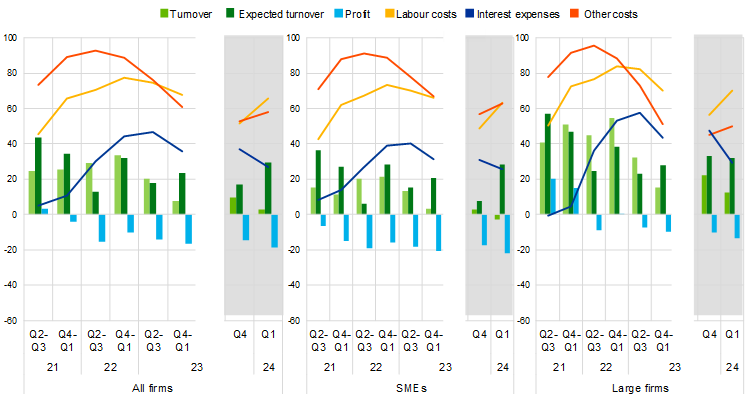

A net 3% of enterprises reported an increase in turnover over the last three months, down from 10% in the previous survey round, but firms were more optimistic regarding developments in the next quarter (Chart 2). At the same time, more firms saw a deterioration in their profits than in the previous survey round (with a net percentage of -19%). The survey shows that cost pressures remain widespread across size classes but are declining somewhat for interest expenses.

Firms expected growth in selling prices and wages to moderate over the next 12 months (Chart 3). Selling prices were expected to increase by 3.3% on average (down from 4.5% in the previous survey round), while the corresponding figure for wages was 3.8% (also down from 4.5% in the previous round).

Firms’ inflation expectations declined, and disagreement about the inflation outlook also moderated (Chart 4). Median expectations for annual inflation in one, three and five years stood at 3.4%, 3.0% and 3.0% respectively, thus declining by 0.7, 0.2 and 0.1 percentage points respectively. For inflation in five years, 49% of firms perceived that the risks to the outlook were tilted to the upside, compared with just 13% who considered that the risks were on the downside.

The report published today presents the main results of the 30th round of the SAFE survey for the euro area. The survey was conducted between 1 February and 12 March 2024 and covered the period from October 2023 to March 2024. Half of the firms were asked about economic and financing conditions over the six-month period from October 2023 to March 2024, while the other half were asked about conditions over the three-month period from January to March 2024. The sample comprised 11,699 enterprises in the euro area, of which 10,704 (91%) had fewer than 250 employees. As of this round, the survey will be conducted on a quarterly basis and will include a new set of quantitative questions on firms’ euro area inflation expectations and expectations about selling prices, wage costs, other input costs and employment.[1]

For media queries, please contact Silvia Margiocco, silvia.margiocco@ecb.europa.eu, tel.: +49 69 1344 6619.

Notes:

- The report on this SAFE survey round, together with the questionnaire and methodological information, is available on the ECB’s website.

- Detailed data series for the individual euro area countries and aggregate euro area results are available on the ECB Data Portal.

Chart 1

Changes in the terms and conditions of bank financing for euro area enterprises

(net percentages of respondents)

Base: Enterprises that had applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. The figures refer to rounds 22 to 30 of the survey (April-September 2020 to January-March 2024).

Notes: Net percentages are the difference between the percentage of enterprises reporting an increase for a given factor and the percentage reporting a decrease. The data included in the chart refer to Question 10 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main chart covers a reference period of six months for the survey questions.

Chart 2

Changes in the income situation of euro area enterprises

(net percentages of respondents)

Base: All enterprises. The figures refer to rounds 23 to 30 of the survey (April-September 2020 to January-March 2024).

Notes: See the notes on Chart 1. The data included in the chart refer to Question 2 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main chart covers a reference period of six months for the survey questions.

Chart 3

Expectations regarding selling prices, wages, input costs and employment one year ahead

(percentage change over the next 12 months)

Base: All enterprises. The figures refer to round 28 (October 2022-March 2023), the first pilot (March-June 2023), round 29 (April-September 2023), the second pilot (October-December 2023) and round 30 (January-March 2024), with firms’ replies collected in the last month of the respective survey waves.

Notes: Euro area firms’ mean and median expectations regarding changes in selling prices, wages of current employees, non-labour input costs and number of employees for the next 12 months, along with interquartile ranges, using survey weights. The statistics are computed after trimming the data at the country-specific 1st and 99th percentiles. The data included in the chart refer to Question 34 of the survey. Questions on non-labour input costs and employees were not available in round 28.

Chart 4

Firms’ expectations about euro area inflation at different horizons

(annual percentages)

Base: All enterprises.

Notes: Survey-weighted medians, modes and interquartile ranges for firms’ expectations about euro area inflation in one, three and five years. Quantiles are computed by linear interpolation of the mid-distribution function.

In preparation for these changes, two pilot rounds were run in June and December 2023 to test the new questions and the new frequency of the survey. The report includes the results of the second pilot, which covered the fourth quarter of 2023. The charts on selling price and inflation expectations report also on the results of the first pilot, covering the second quarter of 2024.

Banca Centrală Europeană

Direcția generală comunicare

- Sonnemannstrasse 20

- 60314 Frankfurt pe Main, Germania

- +49 69 1344 7455

- media@ecb.europa.eu

Reproducerea informațiilor este permisă numai cu indicarea sursei.

Contacte media