Priorities for fiscal policies under the 2019 European Semester

Published as part of the ECB Economic Bulletin, Issue 5/2019.

On 5 June the European Commission issued its 2019 European Semester Spring Package of policy recommendations for EU Member States. The package includes country-specific recommendations (CSRs) for economic and fiscal policies in 2020 for all Member States.[1] It also contains recommendations regarding the implementation of the European Union’s Stability and Growth Pact (SGP) for some countries.[2] With regard to fiscal policies, the recommendations are based on the Commission’s 2019 spring forecast and its assessment of countries’ policy plans as reflected in the updates of the stability and convergence programmes released in April. This box examines the fiscal policy recommendations addressed to the euro area countries. The examination shows that in countries with high levels of government debt, building buffers to strengthen resilience in cyclical downturns remains a priority for fiscal policies. At the same time, countries that have achieved sound fiscal positions could utilise some fiscal space for measures to support economic growth.

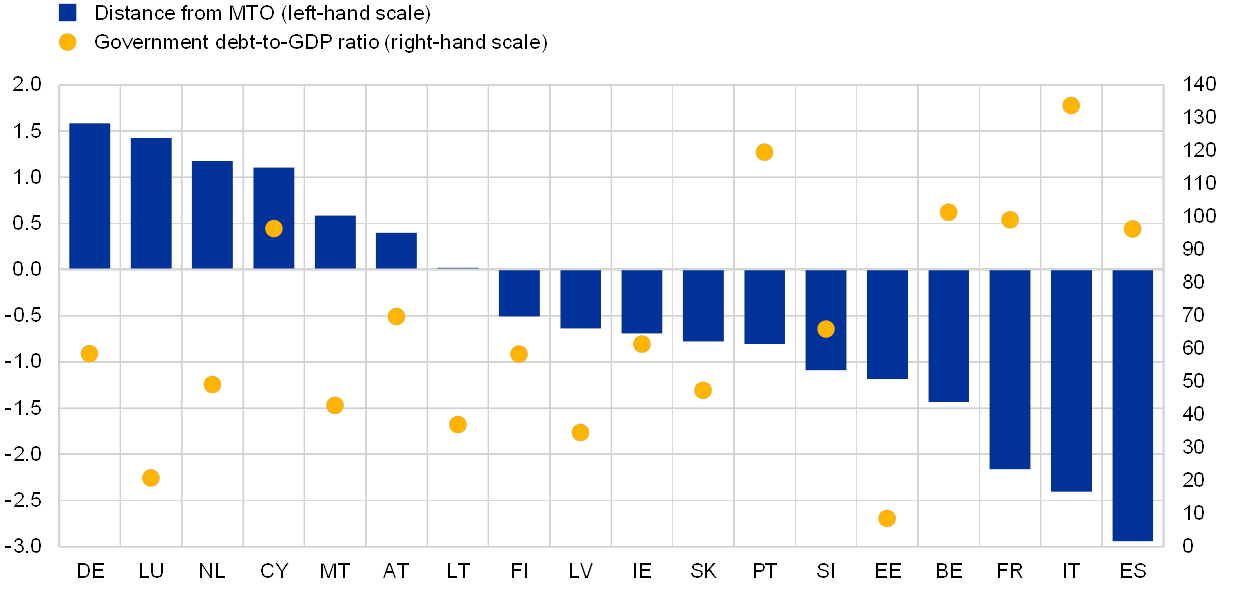

The 2019 Spring Package confirms the pattern of a significant divergence of fiscal positions across countries. According to the European Commission’s 2019 spring forecast, seven euro area countries are assessed to have reached sound fiscal positions with underlying budgetary positions close to or above their medium-term budgetary objectives (MTOs) at the beginning of 2019 (see Chart A). This helps to reduce government debt ratios, provides policy space for measures aimed at raising potential output growth, and bolsters the resilience of public finances ahead of a possible downturn. At the same time, a number of countries are still some distance away from their MTOs, most notably countries with government debt-to-GDP ratios of more than 90%. They remain vulnerable to an economic downturn and financial market volatility.

Chart A

Distance from MTOs and levels of general government debt in 2019

(percentages of GDP)

Sources: European Commission (AMECO database) and ECB calculations.

Notes: The distance from a country’s MTO is measured as the difference between the structural balance and the MTO. Countries no further than 0.25% of GDP from their MTOs are considered to have reached them (see also the 2019 edition of the European Commission’s Vade Mecum on the Stability and Growth Pact). The chart excludes Greece, which does not have an MTO for 2019. Following its exit from the economic adjustment programme, Greece has set an MTO for the period 2020-22.

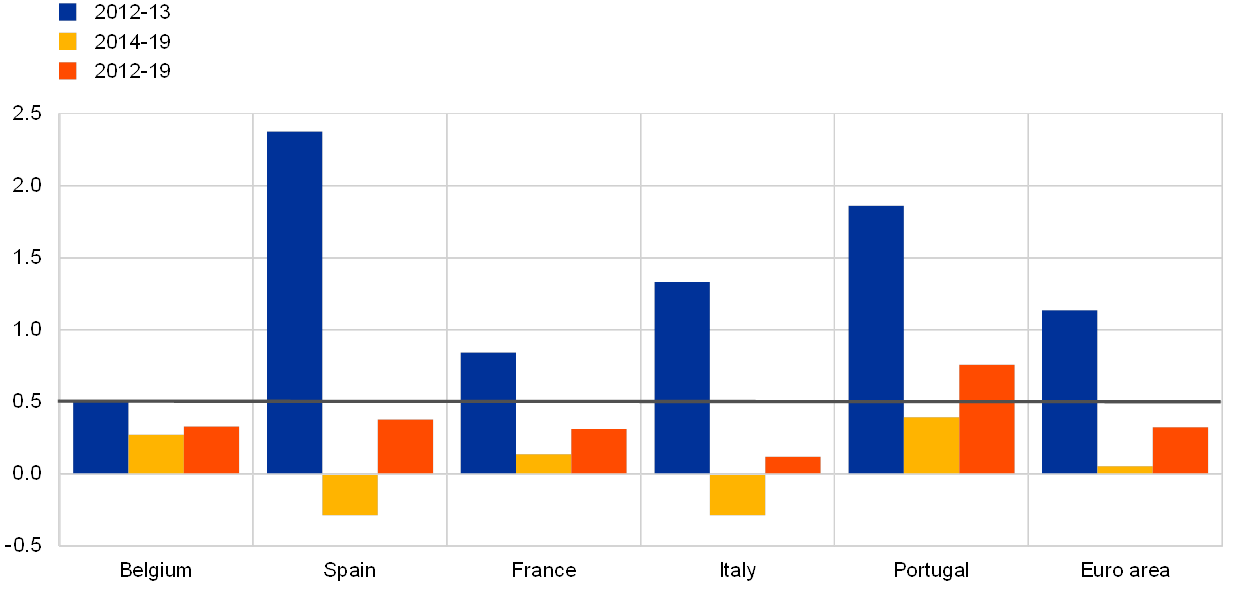

In most cases, the distance from the MTO in countries with high levels of government debt reflects overall limited adjustment progress in recent years. As shown in Chart B, most euro area countries with government debt above 90% of GDP implemented large fiscal adjustments in 2012-13, as measured by the change in the structural balance. This indicator comprises headline budget balances net of the impact of the economic cycle and one-off measures. For some countries with high levels of government debt, the adjustments exceeded the requirements under the SGP, in part reflecting financial market pressures. Thereafter, in the period 2014-19 fiscal adjustment slowed considerably. It remained below the SGP’s benchmark requirement of 0.5% of GDP in all these countries, except Portugal, which has come closest to its MTO within this group (see Chart A).[3] Conversely, the structural budgetary positions of Spain and Italy have deteriorated over recent years, thus widening the gaps vis-à-vis their MTOs. Moreover, the overall limited improvement in structural balances in recent years tends to overstate the efforts actually undertaken by governments. This is because declines in government interest expenditure as a percentage of GDP, as well as revenue windfalls reflecting extraordinary revenue increases during the past economic expansion, have contributed to favourable developments in structural balances.

Chart B

Change in structural balances of countries not at their MTOs and with debt above 90% of GDP

(percentages of GDP)

Sources: European Commission (AMECO database) and ECB calculations.

Notes: The horizontal line refers to the benchmark requirement under the SGP for an annual improvement in the structural balance of 0.5% of GDP. The chart excludes Greece, which did not set an MTO during this period.

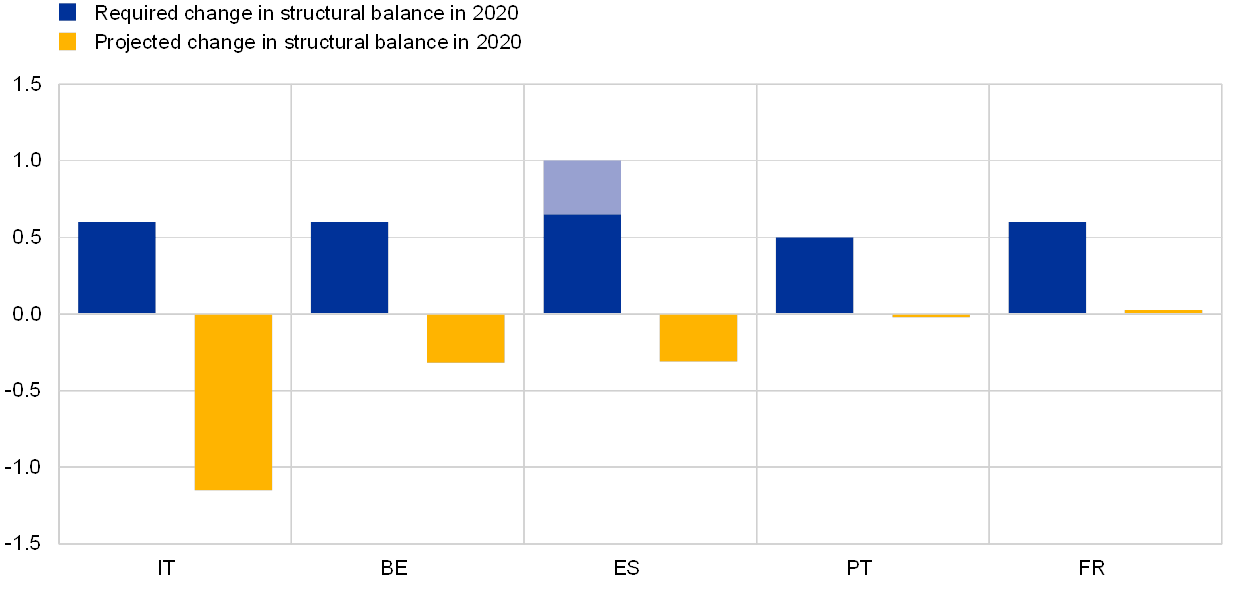

While the CSRs set fiscal policy priorities for 2020 that differ across countries, they all emphasise the need to achieve a more growth-friendly composition of public finances. Countries that have not yet achieved their MTOs are advised to align their fiscal adjustment efforts with the requirements of the SGP. This is consistent with the need for countries with high debt and remaining fiscal gaps to build fiscal buffers that would ensure their resilience if downside risks to the economy materialise. However, it would require sizeable additional fiscal adjustment measures on the part of such countries (see Chart C). Given the asymmetric nature of the SGP, countries that have achieved their MTOs do not receive a recommendation regarding the use of policy space accumulated under its rules. Germany is recommended, “while respecting” the MTO, to “use fiscal and structural policies to achieve a sustained upward trend in private and public investment” which is in line with government plans. Countries with available fiscal space could utilise part of it to support economic growth. Moreover, the recommendations generally emphasise the need for a more growth-friendly composition of public finances to enhance potential output growth, for example, through increasing the quality of investment in infrastructure and education, taking into account differing needs across countries.

On 5 June 2019 the European Commission also issued recommendations for some euro area countries regarding the implementation of the SGP. The Commission adopted reports for Belgium, France, Italy and Cyprus under Article 126(3) of the Treaty on the Functioning of the European Union in which it assesses their compliance with the Treaty’s deficit and debt criteria. In the case of Belgium, the report concludes that at the current juncture it is not possible to fully determine whether the debt criterion is complied with, mainly owing to uncertainty regarding the extent to which an increase in advance corporate income tax payments collected in 2017 and 2018 is of a structural nature. For France, the report concludes that the deficit and debt criteria should be considered as currently complied with. For Italy, the report concluded that a debt-based Excessive Deficit Procedure (EDP) was warranted, after assessing all relevant factors and notably, among them, the non-compliance with the requirement under the SGP’s preventive arm in 2018, the risk of a significant deviation in 2019, and a projected headline deficit above 3% of GDP in 2020. On 3 July 2019 the Commission concluded that an EDP was no longer warranted for Italy at this stage. It took account of the mid-year budget for 2019 as well as a decree-law adopted by the Italian government on 1 July, which provided for an additional structural effort of 0.45% of GDP in 2019. Based on this information, the Commission assessed Italy to be broadly compliant with the requirements under the preventive arm of the SGP in 2019. It stated that it would closely monitor the execution of the amended 2019 budget and would assess the compliance of the 2020 draft budgetary plan with the SGP in the autumn. For Cyprus, the Commission considers that no further steps towards a decision on the existence of an excessive deficit should be taken, despite the deficit having breached the 3% of GDP threshold in 2018 as a result of one-off support to the financial sector. This is because Cyprus exceeded its MTO in 2018 and is projected to be fully compliant with all SGP requirements in 2019 and 2020. Finally, the Commission recommended that the EDP for Spain be abrogated, based on the 2018 budget outcome, and the Economic and Financial Affairs Council adopted a corresponding decision on 14 June 2019.

Chart C

Adjustment requirements under the SGP in 2020 for euro area countries not at their MTOs

(percentage points of GDP)

Sources: European Commission (AMECO database) and ECB calculations.

Notes: The structural effort requirements for each year are enshrined in the CSRs. For 2020, they are quantified in the CSRs for fiscal policies under the 2019 European Semester. The area shaded light blue within the bar for Spain reflects the fact that the agreed adjustment requirement is lower than foreseen under the preventive arm matrix. The Commission forecast for 2020 is based on a “no policy change” scenario, as countries’ budgets for that year are not yet available.

Looking ahead, the forthcoming review of the changes to the EU fiscal framework conceived during the economic and financial crisis (the “two-pack” and “six-pack” legislative packages) should be used to strengthen the incentives for building fiscal buffers in good times. First, it would be useful to review the EDP procedure with a view to better promoting the achievement of structural (rather than nominal) adjustment requirements under the corrective arm of the SGP. Second, the effectiveness of the SGP’s debt rule in reducing government debt towards sound levels should be improved, thus strengthening the role of the debt-to-GDP ratio as an anchor of the fiscal framework. Third, for the credibility of the fiscal surveillance exercise, it is important that predictability is increased such that clearer conclusions can be reached regarding compliance with the rules. In this context, the assessment of compliance with the requirements under the preventive arm of the SGP should be reviewed. This includes situations in which the achievement of adjustment requirements under the expenditure rule[4] and the structural balance approach leads to conflicting signals.

- See also the box entitled “Country-specific recommendations for economic policies under the 2019 European Semester” in this issue of the Economic Bulletin.

- The CSRs were finalised and adopted by the Economic and Financial Affairs Council on 9 July 2019.

- According to the 2019 stability and convergence programmes, a few countries have updated their MTOs. Luxembourg has raised its MTO for 2020 by 1 percentage point and Italy’s has been raised by 0.5 percentage points. In contrast, Portugal, Slovenia and Slovakia have lowered their MTOs for 2020.

- The expenditure rule is based on an expenditure aggregate which excludes interest spending, expenditure on EU programmes fully matched by EU funds revenue, and cyclical elements of unemployment benefit expenditure (for details, see the 2019 edition of the European Commission’s Vade Mecum to the Stability and Growth Pact). Countries that have not yet achieved their MTOs must ensure that this expenditure aggregate grows at a rate below a multi-annual reference rate of potential output growth. Any growth in the expenditure aggregate that exceeds this reference rate must be matched by discretionary revenue measures that yield additional tax revenue.