Cyclical developments in the euro area current account

Published as part of the ECB Economic Bulletin, Issue 5/2018.

The euro area current account balance stood at the historically high level of 3.6% of GDP in the year up to the first quarter of 2018, slightly above the level of 3.5% of GDP recorded one year earlier (see Chart A). The slight increase in the current account surplus however masks significant decreases in the surplus on trade in goods (by 0.2 percentage point of GDP) as well as in the surplus on primary income (by 0.3 percentage point of GDP), which were slightly more than offset by an increase in the surplus on trade in services (by 0.5 percentage point of GDP).

Chart A

Main components of the euro area current account balance

(percentage of GDP, four-quarter moving sum)

Source: ECB.

Note: The latest observation is for the first quarter of 2018.

There are, however, signs of a stabilisation of the current account balance, albeit at elevated levels, largely on account of developments in the oil price cycle (see Chart B). The current account surplus had reached a record high – slightly above its current level – in the third quarter of 2016. This peak coincided with an all-time low in the energy trade deficit at the end of 2016 due to the trough in oil prices a few months earlier. Since then, the energy trade balance has worsened by 0.3 percentage point of GDP. This, together with a slight decrease in the surpluses on non-energy trade in goods as well as on primary income, more than offset the increase in the surplus on trade in services over the same period. Looking at energy trade developments over a longer period, the stabilisation in oil prices after 2012 and their subsequent fall from 2014 to the end of 2015 had in fact reduced the energy trade deficit by about 2 percentage points of GDP and thus entirely accounted for the rise in the current account surplus over the same period. The current account balance of the euro area excluding energy trade, in turn, has remained remarkably stable since 2013.

Chart B

Energy trade balance, non-energy current account balance and oil prices

(percentage of GDP, four-quarter moving sum; USD per barrel)

Sources: ECB and Eurostat.

Note: The latest observation is for the first quarter of 2018.

From a saving/investment perspective, the stabilisation of the current account surplus largely reflects a reduction in net lending by the private sector which is however offset by an increase in saving of the public sector (see Chart C). Since the start of the economic recovery in 2013, private sector investment has been steadily recuperating, albeit at a slow pace, while gross saving of the private sector only levelled off in 2016 and started to decline in 2017. As a result, net lending of the private sector declined in both 2016 and 2017. This development was however largely offset by a further reduction in net borrowing of the public sector due to the ongoing fiscal consolidation efforts in a number of countries.

Chart C

Euro area gross saving and investment

(percentage of GDP)

Source: European Commission.

Note: The latest observation is for 2017.

From the perspective of euro area imbalances, the stabilisation of the euro area current account surplus reflects to some extent current account adjustment in euro area countries (see Chart D). In fact, the contribution of Germany to the current account surplus of the euro area has shrunk by about 0.3 percentage point of euro area GDP since the beginning of 2016. This development has contrasted with a further rise in the current account surplus of the Netherlands, by about 0.2 percentage point of euro area GDP over the same period, which was however broadly offset by a narrowing of current account surpluses of other euro area economies. At the same time, programme and post-programme surveillance countries, on aggregate, continued to record further improvements in their current account balances of around 0.2 percentage point of GDP.

Chart D

Current account balance of the euro area and selected euro area countries

(percentage of GDP, four-quarter moving sum)

Source: ECB.

Notes: The latest observation is for the first quarter of 2018. PPS stands for post-programme surveillance.

At present, the position of the euro area in the business cycle, together with the recent increase in oil prices, should further support the stabilisation of the current account balance. A weaker cyclical position of the euro area compared with its main trading partners continues to weigh on euro area import demand, while supporting foreign demand for euro area exports. This leads to a temporary increase in the euro area’s trade surplus and thereby its current account balance. In fact, a fraction of the current account surplus of about 0.1 percentage point of GDP is estimated to be due to the position of the euro area in the business cycle relative to that of its main trading partners, based on standard elasticities available in the empirical literature. This implies that the current account surplus of the euro area would decline by around 0.1 percentage point of GDP over the medium term if the output gaps of the euro area and its main trading partners were to converge. A similar fraction of about 0.1 percentage point of GDP of the current account surplus, in turn, can be attributed to the deviation of oil prices from their trend level. As a result, the cyclically adjusted current account balance of the euro area is about 0.2 percentage point below its current level.[1]

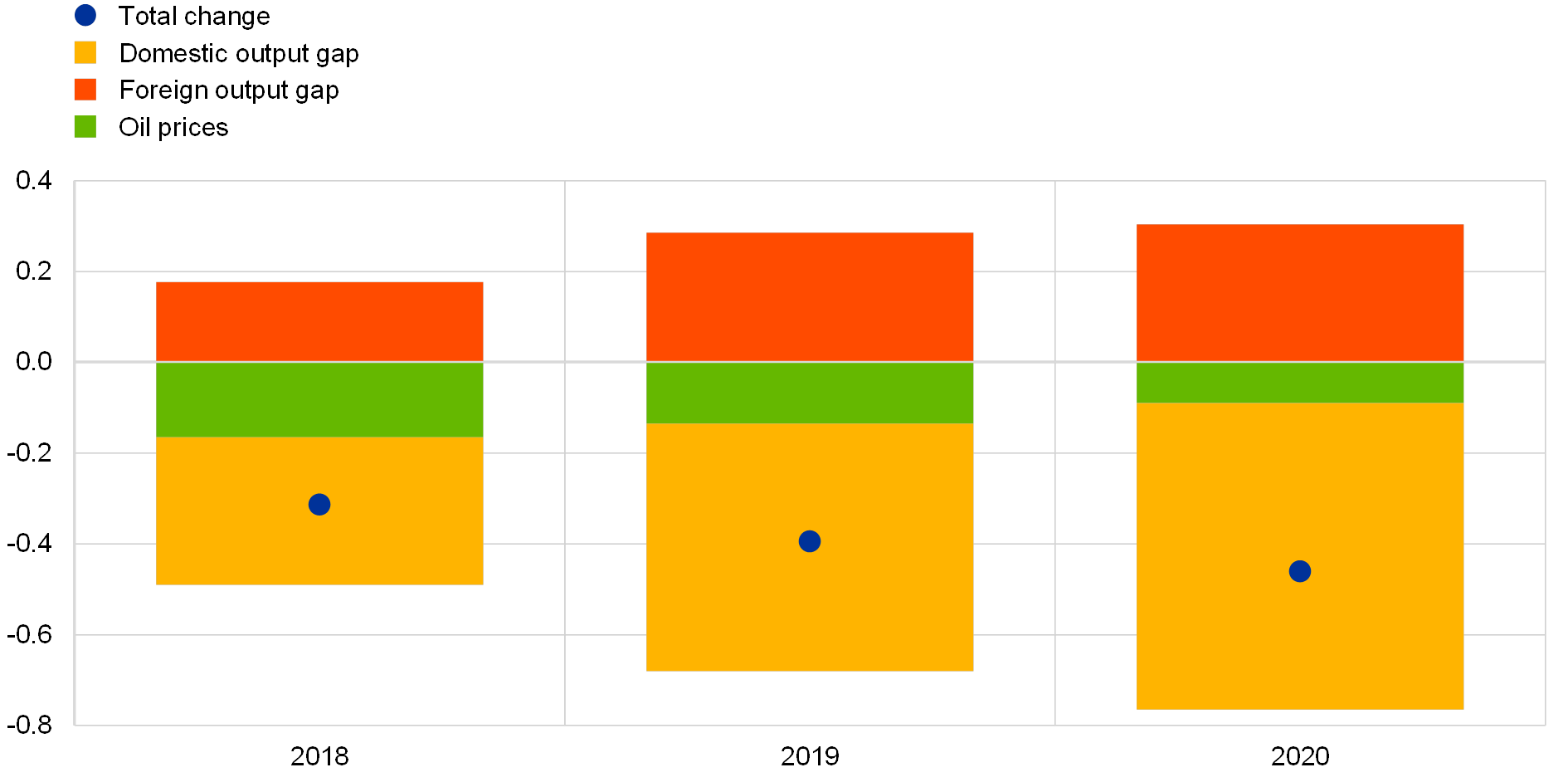

Chart E

Simulated change in the current account balance due to projected output gap and oil price developments

(percentage points of GDP)

Sources: ECB, IMF and ECB staff estimates.

Notes: Calculations are based on the June 2018 Eurosystem staff macroeconomic projections for the domestic output gap and the IMF’s April 2018 World Economic Outlook for the foreign output gap.

Looking ahead, the ongoing euro area rebalancing, as well as developments in the euro area business cycle together with fluctuations in oil prices, should contribute to a narrowing of the current account surplus (see Chart E). Oil price projections – increasing markedly in 2018 and decreasing somewhat again over the remainder of the projection horizon to hover around their trend level – imply, based on standard elasticities, a narrowing of the euro area current account surplus by between 0.1 and 0.2 percentage point of GDP by the end of 2020. At the same time, the narrowing of the negative output gap in the euro area – turning positive in 2018 and projected to further increase over the coming years – should increase import demand and thereby reduce the euro area current account surplus. Based on standard elasticities, the impact would range between 0.3 percentage point of GDP in 2018 and 0.7 percentage point of GDP by the end of 2020. However, the effect of the increasingly positive output gap in the euro area is partly – although not fully – offset by a similar but less pronounced improvement in the global output gap, which is expected to add up to 0.3 percentage point of GDP to euro area foreign demand and thereby support the current account surplus. As a result of these two opposing forces, the combined effect of oil price and business cycle factors would amount to a reduction of the euro area current account surplus by between 0.3 percentage point of GDP in 2018 and 0.5 percentage point of GDP by the end of 2020. These effects are consistent with the June 2018 Eurosystem staff macroeconomic projections, which include a decrease in the current account surplus by around one percentage point of GDP over the same horizon, implying that in addition to cyclical factors also structural factors are expected to contribute to a narrowing of the current account balance.

- These estimates are based on standard elasticities for the current account balance with respect to the output gap (expressed relative to that of the rest of the world) and the oil price (interacted with the energy trade balance), respectively. Estimates range between 0.4 and 0.5 for the former and between 0.5 and 0.6 for the latter, as for instance in Phillips et al., “The External Balance Assessment (EBA) Methodology”, IMF Working Paper 13/272, 2013, and Zorell, N., “Large net foreign liabilities of euro area countries”, Occasional Paper Series, No 198, ECB, 2017.

Banque centrale européenne

Direction générale Communication

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Allemagne

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction autorisée en citant la source

Contacts médias